Introduction

When it comes to planning for your financial future, few decisions are as personal—or as powerful—as choosing the right indexed insurance strategy. Whether you’re just starting to grow your wealth or you’ve been building a business for years, the question remains: Should I choose a conservative or aggressive indexed plan?

As women entrepreneurs, we wear many hats—visionary, leader, caretaker, risk-taker. Our financial strategies must align not just with our businesses, but with our dreams, our responsibilities, and the legacy we want to leave. That’s why understanding the difference between conservative and aggressive indexed plans is crucial to building a future that feels both secure and abundant.

In this article, we’ll explore the key differences between conservative and aggressive indexed plans, break down the pros and cons of each, and help you determine which one aligns with your values, goals, and stage of life.

Understanding Indexed Plans

First, a quick refresher: Indexed universal life insurance (IUL) plans are a form of permanent life insurance that link cash value growth to the performance of a stock market index—most commonly, the S&P 500. But here’s the key: your money isn’t directly invested in the market. Instead, it benefits from market gains while being protected from losses due to market downturns.

What sets indexed plans apart is the flexibility: you can structure them to be either more conservative (with safety and modest growth in mind) or more aggressive (targeting higher returns with greater volatility).

These options are designed to give you control over how your money grows—and how it’s protected.

What does conservative mean in indexed life planning?

A conservative indexed strategy focuses on protecting your cash value and prioritizing long-term stability. Typically, it includes:

- Lower caps and higher floors (e.g., a 0% floor and a 6-8% cap).

- Fixed interest accounts or index accounts with strong downside protection.

- Smoother performance during market fluctuations.

- A focus on stability, especially if you’re close to retirement or using the plan for legacy or income planning.

Women who opt for conservative indexed plans often do so because they value predictable growth, minimal risk, and a steady financial strategy that aligns with their family or retirement goals.

Best for:

- Those closer to retirement

- Business owners who want stable income streams

- Anyone risk-averse or planning for future generations

What does “aggressive” mean in an indexed plan?

On the other hand, an aggressive indexed strategy targets higher potential returns with the understanding that it may also come with greater short-term fluctuations.

Aggressive plans often include:

- Higher caps and participation rates (e.g., 10-15% cap or uncapped strategies with spreads).

- Strategies tied to multiple indices, such as global markets or volatility-controlled indexes.

- More complexity, but greater potential for growth in strong market years.

These plans appeal to entrepreneurial women who are comfortable with some risk, are still in their wealth-building years, or want to take full advantage of market momentum without directly investing in equities.

Best for:

- Those who can handle some risk for the potential of higher returns

- Younger women with longer investment horizons

- Entrepreneurs still scaling their businesses

What does your financial DNA say?

Choosing between conservative and aggressive indexed strategies isn’t just about numbers—it’s about who you are.

Ask yourself:

- Do I lose sleep when markets dip?

- Am I more focused on protecting what I’ve built or growing it further?

- Do I need to access this money soon—or can it sit and grow?

Your answers will guide the structure of your indexed plan.

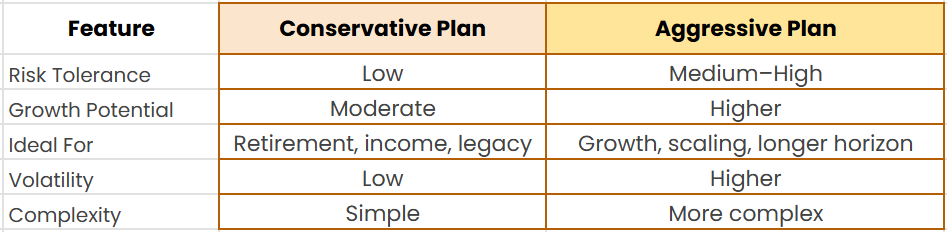

Comparing the Features

Case Study: Claire X Maria

Let’s meet two real-world examples:

Claire, 48:

A business coach and mother of two, Claire is focused on preparing for retirement in the next 10-15 years. She values steady growth and prefers a plan with guaranteed floors and stable annual performance. Claire chooses a conservative indexed plan with a high floor and moderate cap.

Maria, 35:

Maria runs a marketing agency and is reinvesting in her business while building wealth for the long term. She’s comfortable with risk, especially if it means higher returns. She opts for an aggressive indexed plan with a wider cap and multiple indexing options.

Both women are making the right choice—for their stage of life, their values, and their vision of the future.

When to switch strategies

One of the beautiful things about indexed strategies is their flexibility. Many indexed plans allow for changes down the road.

You might start aggressively, then shift to conservative as you approach retirement. Or you might take a conservative approach until your income stabilizes, then gradually adjust for growth.

Life isn’t static—and your financial strategy shouldn’t be either.

Compounding: secret power

Whether you go conservative or aggressive, the most important ingredient is time. Compound interest is your best friend.

Let’s say you allocate $10,000 a year into your indexed plan.

- At a conservative 5% average return, that grows to $132,000 in 10 years.

- At a more aggressive 8% return, it becomes $156,000.

Stretch that to 20 years, and the difference is even more profound:

- 5% return = $330,000

- 8% return = $457,000

The takeaway? The earlier you start—and the more consistently you contribute—the more your plan can work for you.

Common misconseptions to avoid

Let’s clear up a few myths:

❌ Myth: Aggressive = unsafe

✅ Truth: You’re still protected from market losses. Even aggressive strategies use floors to shield your downside.

❌ Myth: Conservative = no growth

✅ Truth: Conservative strategies often outperform bank savings and CDs with less volatility.

❌ Myth: I need to be rich to start

✅ Truth: Many indexed plans are accessible with flexible premiums.

Final thoughts: building with intention

Whether you choose conservative or aggressive—or a mix of both—indexed plans offer a rare balance of growth and protection. They allow you to dream big while planning smart. And most importantly, they honor the complexity of your life and goals as a woman entrepreneur.

At Alyena Wealth, we believe that financial empowerment is personal. That’s why we tailor every recommendation to your journey—whether that means playing it safe, reaching for more, or adjusting along the way.

– Ready to choose your plan? –

Your ideal plan isn’t just about numbers—it’s about clarity, confidence, and alignment.

Let’s figure it out together. Schedule your free consultation today and explore the strategy that fits your future best. Whether you’re drawn to protection, growth, or a balance of both, we’re here to help.

📩 Click the link to get started: https://calendly.com/alyenawealth/first-meeting . You’re not just growing financially—you’re creating a legacy!